from SouthGobi Resources Ltd. (HKG:1878)

SouthGobi Announces Fourth Quarter and Full Year 2025 Financial and Operating Results

HONG KONG, HK / ACCESS Newswire / March 27, 2026 / SouthGobi Resources Ltd. (Hong Kong Stock Exchange ("HKEX"): 1878, TSX Venture Exchange ("TSX-V"): SGQ) (the "Company" or "SouthGobi") today announces its financial and operating results for the quarter and year ended December 31, 2025. All figures are in U.S. dollars ("USD") unless otherwise stated.

The Board of Directors (the "Board") wish to inform that the Company's independent auditors, BDO Limited, have completed their audit of the consolidated financial statements of the Company for the year ended December 31, 2025 in accordance with IFRS Accounting Standards as issued by the International Accounting Standards Board ("IFRS Accounting Standards") and would like to announce the audited annual results of the Company for the year ended December 31, 2025 together with the comparative figures for the previous year and the respective notes in this announcement.

Significant Events and Highlights

The Company's significant events and highlights for the year ended December 31, 2025 and the subsequent period to March 27, 2026 are as follows:

Operating Results - The Company increased the scale of its mining operations since 2024, as well as implementing various coal processing methods, including screening, wet washing and dry coal processing, which have resulted in improved coal quality and enhanced production volume and growth of coal export volume into China during the year.

In response to the market demand for different coal products, the Company focused on expanding the categories of coal products in its portfolio, including mixed coal, wet washed coal and dry processed coal. In addition, the Company has experienced success with processing its inventory of F-grade coal products through cost-effective screening procedures. As a result of the improvement in the quality of the processed F-grade coal, the Company was able to meet the import coal quality standards established by Chinese authorities and has been exporting this product to China for sale since the first quarter of 2024, further enhancing the Company's coal export volume.

The Company recorded sales volume of 11.2 million tonnes in 2025 compared to 7.0 million tonnes in 2024, while the Company recorded an average realised selling price of $53.5 per tonne in 2025 compared to $70.4 per tonne in 2024. The decrease in the average realised selling price was mainly due to the Company facing headwinds in the China coal market since 2024, leading to the Company changing its product mix to sell a greater percentage of lower-priced coal products.

Financial Results - The Company recorded a $133.2 million loss from operations in 2025 compared to a $153.9 million profit from operations in 2024. The financial results were impacted by the decreased average realised selling price in 2025 as compared to 2024, the change in product mix year-over-year (as the Company sold more processed coal with higher production costs) and impairment losses on coal stockpile and items of property, plant and equipment of $77.3 million and $42.0 million were recorded respectively in 2025.

Notice from Mongolian Government Plenipotentiary and designation of Company's mining deposits as mineral deposits of strategic importance - On April 2, 2025, SouthGobi Sands LLC ("SGS") received a letter from a plenipotentiary representative of the Mongolian government (the "Letter") which invited SGS to participate in negotiations in relation to determining the Mongolian state's ownership interest in SGS, being the legal entity which holds the Company's coal mining and exploration licenses in Mongolia.

The Letter states that, in furtherance of Mongolia's National Wealth Fund Law which was passed in April 2024, the Mongolian government resolved on February 5, 2025 to appoint a plenipotentiary representative (the "Plenipotentiary Representative of the Mongolian Government") to negotiate with legal persons holding a mining license for a deposit designated by the Mongolian government as a strategically important deposit ("Mineral Deposits of Strategic Importance") in relation to determining the proportionate interest the Mongolian state has in such legal entity or whether to replace the Mongolian state's interest with a royalty interest.

The Company has been advised by its Mongolian legal counsel that, the Government of Mongolia is empowered to participate on an equity ownership basis with the license holder in the exploitation and/or mining of each Mineral Deposit of Strategic Importance on terms to be negotiated between the Government of Mongolia and such license holder. Based solely on the knowledge of the Company's Mongolian legal counsel, the Company is aware that various other license holders of Mineral Deposits of Strategic Importance have entered into similar negotiations with the Plenipotentiary Representative of the Mongolian Government. The Company also understands that any legal person holding a special licence for a Mineral Deposit of Strategic Importance shall not, individually or jointly with other entities having a common interest, hold more than 34% of the total issued and outstanding shares of such legal person. However, there is uncertainty as to how these regulations will be interpreted and applied to a publicly-listed company which is the beneficial owner of a Mineral Deposit of Strategic Importance. In the event that the aforementioned ownership restriction is not complied with, the Government of Mongolia shall have the right to appoint a Plenipotentiary Representative to take charge of managing such legal person to ensure legal compliance.

On April 24, 2025, SGS initiated preliminary discussions with the Plenipotentiary Representative of the Mongolian Government. The Company anticipates that the discussion between SGS and the Plenipotentiary Representative of the Mongolian Government will continue and both parties will endeavour to engage in good faith for the purpose of arriving at a mutual and constructive understanding and agreement. The Company intends to fully cooperate with the Mongolian government and provide all necessary information to the extent permitted by applicable law.

As at the date of this press release, the deposits covered by four of the Company's Mongolian mining licenses have been designated as Mineral Deposits of Strategic Importance by Mongolian government authorities. The relevant mining licenses relate to the Company's Ovoot Tolgoi Mine and the Soumber Deposit.

2025 March Deferral Agreement - On March 20, 2025, the Company and JD Zhixing Fund L.P. ("JDZF") entered into a deferral agreement (the "2025 March Deferral Agreement") pursuant to which JDZF agreed to grant the Company a deferral of (i) the cash and payment-in-kind interest ("PIK Interest"), management fees, and related deferral fees in the aggregate amount of approximately $111.6 million which will be due and payable to JDZF on or before August 31, 2025 pursuant to the deferral agreement dated March 19, 2024 and the deferral agreement dated April 30, 2024; (ii) semi-annual cash interest payment of approximately $7.9 million payable to JDZF on May 19, 2025 under the Convertible Debenture; (iii) semi-annual cash interest payments of approximately $8.1 million payable to JDZF on November 19, 2025 and the $4.0 million in PIK Interest payable to JDZF on November 19, 2025 under the Convertible Debenture; and (iv) management fees in the aggregate amount of approximately $6.1 million payable to JDZF on May 16, 2025, August 15, 2025, November 15, 2025 and February 15, 2026, respectively, under the amended and restated mutual cooperation agreement (the "Amended and Restated Cooperation Agreement") (collectively, the "2025 March Deferred Amounts").

The effectiveness of the 2025 March Deferral Agreement and the respective covenants, agreements and obligations of each party under the 2025 March Deferral Agreement was subject to the Company obtaining the requisite approval of the 2025 March Deferral Agreement from shareholders in accordance with the requirements of applicable Canadian securities laws and Rule 14.33 and Rule 14A.36 of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited (the "Listing Rules"). The 2025 March Deferral Agreement was approved by the Company's disinterested shareholders at the annual general meeting ("AGM") of shareholders convened on June 27, 2025.

The principal terms of the 2025 March Deferral Agreement are as follows:

Payment of the 2025 March Deferred Amounts will be deferred until August 31, 2026 (the "2025 March Deferral Agreement Deferral Date").

As consideration for the deferral of the 2025 March Deferred Amounts which relate to the payment obligations arising from the Convertible Debenture, the Company agreed to pay JDZF a deferral fee equal to 6.4% per annum on the outstanding balance of such 2025 March Deferred Amounts, commencing on the date on which each such 2025 March Deferred Amounts would otherwise have been due and payable under the Convertible Debenture.

As consideration for the deferral of the 2025 March Deferred Amounts which relate to payment obligations arising from the Amended and Restated Cooperation Agreement, the Company agreed to pay JDZF a deferral fee equal to 1.5% per annum on the outstanding balance of such 2025 March Deferred Amounts commencing on the date on which each such 2025 March Deferred Amounts would otherwise have been due and payable under the Amended and Restated Cooperation Agreement.

The 2025 March Deferral Agreement does not contemplate a fixed repayment schedule for the 2025 March Deferred Amounts or related deferral fees. Instead, the 2025 March Deferral Agreement requires the Company to use its best efforts to pay the 2025 March Deferred Amounts and related deferral fees due and payable under the 2025 March Deferral Agreement to JDZF. During the period beginning as of the effective date of the 2025 March Deferral Agreement and ending as of the 2025 March Deferral Agreement Deferral Date, the Company will provide JDZF with monthly updates of its financial status and business operations, and the Company and JDZF will on a monthly basis discuss and assess in good faith the amount (if any) of the 2025 March Deferred Amounts and related deferral fees that the Company may be able to repay to JDZF, having regard to the working capital requirements of the Company's operations and business at such time and with the view of ensuring that the Company's operations and business would not be materially prejudiced as a result of any repayment.

If at any time before the 2025 March Deferred Amounts and related deferral fees are fully repaid, the Company proposes to appoint, replace or terminate one or more of its chief executive officer, its chief financial officer or any other senior executive(s) in charge of its principal business function or its principal subsidiary, the Company will first consult with, and obtain written consent (such consent shall not be unreasonably withheld) from JDZF prior to effecting such appointment, replacement or termination.

On March 23, 2026, the Company and JDZF entered into a subsequent deferral agreement with respect to the 2025 March Deferred Amounts. Refer below under the heading entitled "2026 March Deferral Agreement".

Additional Tax and Tax Penalty Imposed by the Mongolian Tax Authority ("MTA") - On July 18, 2023, SGS received an official notice (the "Notice") issued by the MTA stating that the MTA had completed a periodic tax audit (the "Audit") on the financial information of SGS for the tax assessment years between 2017 and 2020, including transfer pricing, royalty, air-pollution fee and unpaid tax payables. As a result of the Audit, the MTA notified SGS that it is imposing a tax penalty against SGS in the amount of approximately $75.0 million. The penalty mainly relates to the different view on the interpretation of tax law between the Company and the MTA. Under Mongolian law, the Company had a period of 30 days from the date of receipt of the Notice to file an appeal in relation to the Audit. Subsequently the Company engaged an independent tax consultant in Mongolia to provide tax advice and support to the Company and filed an appeal letter in relation to the Audit with the MTA in accordance with Mongolian laws on August 17, 2023.

On February 8, 2024, SGS received notice from the Tax Dispute Resolution Council ("TDRC") which stated that, after the TDRC's review, the TDRC issued a decision in relation to SGS' appeal of the Audit, and ordered that the audit assessments set forth in the Notice of July 18, 2023 be sent back to the MTA for review and re-assessment.

On February 22, 2024, SGS received another notice from the MTA stating that the MTA anticipated commencing the re-assessment process on or about March 7, 2024 and the duration of such process will be approximately 45 working days.

On May 15, 2024, SGS received a notice (the "Revised Notice") from the MTA regarding the re-assessment result on the Audit (the "Re-assessment Result"). The re-assessed amount of the tax penalty is approximately $80.0 million. In accordance with applicable Mongolian laws, SGS is entitled to file an appeal to the TDRC regarding the Re-assessment Result within a 30-day period from the date of receiving the Revised Notice.

On June 12, 2024, following consultation with its independent tax consultant in Mongolia, SGS submitted an appeal letter to the TDRC regarding the Re-assessment Result, in accordance with applicable Mongolian laws.

On January 10, 2025, SGS received a resolution dated December 19, 2024 (the "Resolution") from the TDRC in response to the appeal letter sent by SGS to the TDRC on June 12, 2024, relating to the Re-assessment Result. As set forth in the Resolution, the TDRC has determined to reduce the re-assessed amount of tax penalty against SGS from approximately $80.0 million to approximately $26.5 million (the "Revised Re-assessment Result"). In accordance with applicable Mongolian laws, SGS is entitled to file an appeal to the Administrative Court of First Instance in Ulaanbaatar, Mongolia (the "Administrative Court of First Instance") regarding the Revised Re-assessment Result within a 30-day period from the date of receiving the Resolution. After careful consideration and consultation with the Company's independent tax consultant in Mongolia, the Company has determined not to pursue a further appeal of the Revised Re-assessment Result with the Administrative Court of First Instance.

On March 19, 2025, SGS received correspondence from the Administrative Court of First Instance requesting supplemental information regarding a court proceeding initiated by certain officers of the MTA (the "MTA Officials") against the TDRC. Upon further enquiry, SGS obtained a copy of an order dated March 7, 2025 issued by the Administrative Court of First Instance regarding commencement of court proceedings brought by the MTA Officials. The MTA Officials petitioned the court to overturn the TDRC's ruling that reduced SGS's tax penalty from approximately $80.0 million to approximately $26.5 million (the "Proposed Case").

On April 25, 2025, SGS obtained a copy of an order dated April 15, 2025 (the "Latest Court Order") issued by the Administrative Court of First Instance refusing to accept the Proposed Case. According to the Latest Court Order, the Proposed Case was dismissed by the Administrative Court of First Instance. According to applicable Mongolian laws, the plaintiff is entitled to file an appeal to the appellate court, and the Company understood that the MTA Officials, as plaintiff in the Proposed Case, filed an appeal.

On June 9, 2025, SGS obtained a copy of a judgement dated May 27, 2025 (the "Appellate Court Judgement") issued by the Appellate Court for Administrative in Ulaanbaatar, Mongolia (the "Appellate Court"). As per the Appellate Court Judgement, the Appellate Court upheld the court order issued by the Judge of the Administrative Court of First Instance on April 15, 2025. As a result, the claim brought by the MTA Officials against the TDRC in an attempt to dispute or overturn the previous decision made by the TDRC regarding the Re-assessment Result has been dismissed and rejected. According to applicable Mongolian law, the Appellate Court Judgement shall be final and is not subject to further appeal.

In the prior year, the Company recorded an additional tax and tax penalty in the amount of $45.5 million, which consists of a tax penalty payable of $26.5 million and a provision for additional late tax penalty of $19.0 million. As a result of the Revised Re-assessment Result, the Company recorded a reversal of additional tax and tax penalty of $48.5 million in 2024. To date, the Company has paid the MTA an aggregate of $22.2 million in relation to the aforementioned tax penalty. The Company anticipates paying down the outstanding amount of the tax and tax penalty from cash generated from operations in the normal course. According to Mongolian tax law, the MTA has a legal authority to demand payment of the outstanding amount of the Revised Re-assessment Result from the Company at its discretion.

Bank Loan - On October 7, 2025, SGS has entered into a bank loan (the "2025 Bank Loan") for a principal amount of up to RMB235 million (equivalent to approximately $33.1 million) from Khan Bank JSC (the "Bank") with the key commercial terms as follows:

Maturity date set at 18 months from drawdown (the "Term");

Interest rate of 10% per annum on the outstanding principal and interest is calculated on a 365-day year basis;

Loan repayments will consist of interest-only payments during the initial 12 months of the Term, followed by principal amortisation payments during months 13 to 18 of the Term;

Certain items of property, plant and equipment with carrying amount of $2.2 million, land-use rights and intangible assets were pledged as security for the 2025 Bank Loan; and

The Company intends to use the proceeds of the 2025 Bank Loan to support working capital, operating expenses, taxes and the settlement of accounts payable of SGS.

Lawsuit - In January 2014, Siskinds LLP, a Canadian law firm, filed a class action (the "Class Action") against the Company, certain of its former senior officers and directors, and its former auditors (the "Former Auditors"), in the Ontario Court in relation to the Company's restatement of certain financial statements previously disclosed in the Company's public fillings (the "Restatement").

To commence and proceed with the Class Action, the plaintiff was required to seek leave of the Court under the Ontario Securities Act (the "Leave Motion") and certify the action as a class proceeding under the Ontario Class Proceedings Act. The Ontario Court rendered its decision on the Leave Motion on November 5, 2015, dismissing the action against the former senior officers and directors and allowing the action to proceed against the Company in respect of alleged misrepresentation affecting trades in the secondary market for the Company's securities arising from the Restatement. The action against the Former Auditors was settled by the plaintiff on the eve of the Leave Motion.

Both the plaintiff and the Company appealed the Leave Motion decision to the Ontario Court of Appeal. On September 18, 2017, the Ontario Court of Appeal dismissed the Company's appeal of the Leave Motion to permit the plaintiff to commence and proceed with the Class Action. Concurrently, the Ontario Court of Appeal granted leave for the plaintiff to proceed with their action against the former senior officers and directors in relation to the Restatement.

The Company filed an application for leave to appeal to the Supreme Court of Canada in November 2017, but the leave to appeal to the Supreme Court of Canada was dismissed in June 2018.

In December 2018, the parties agreed to a consent Certification Order, whereby the action against the former senior officers and directors was withdrawn and the Class Action would only proceed against the Company, creating the class plaintiffs (the "Class Plaintiffs") and permitting the Class Plaintiffs to proceed with the Class Action against only the Company.

Counsel for the plaintiffs and defendant have: (i) completed document production and oral examinations for discovery; (ii) served expert reports on liability and damages; and (iii) designed a mediation process and finalised, with the participation of the relevant Company's insurers, the mediation under the guidance of former Chief Justice of Ontario George Strathy, which mediation was held and completed on August 11, 2025 (the "Mediation").

As a result of the Mediation, the Class Plaintiffs and the Company have conditionally settled (the "Settlement") the Class Action for CA$6.8 million, including all liability and class counsel fees, notice and administrative costs, fees, costs and expenses related to the litigation and the settlement (the "Settlement Payments"). The Settlement Payments are the obligation of the Company's insurers as of January 2014.

The Settlement was approved by Justice Morgan of the Ontario Superior Court of Justice on December 2, 2025. No appeals have been filed and the time to file an appeal has expired.

2026 March Deferral Agreement - On March 23, 2026, the Company and JDZF entered into an agreement (the "2026 March Deferral Agreement") pursuant to which JDZF agreed to grant the Company a deferral of (i) the cash and PIK Interest, management fees, and related deferral fees in the aggregate amount of approximately $140.5 million which will be due and payable to JDZF on or before August 31, 2026 pursuant to the deferral agreement dated March 20, 2025; (ii) semi-annual cash interest payment of approximately $7.9 million payable to JDZF on May 19, 2026 under the Convertible Debenture; (iii) semi-annual cash interest payments of approximately $8.1 million payable to JDZF on November 19, 2026 and the $4.0 million in PIK Interest payable to JDZF on November 19, 2026 under the Convertible Debenture; and (iv) management fees in the aggregate amount of approximately $7.6 million payable to JDZF on May 16, 2026, August 15, 2026, November 15, 2026 and February 15, 2027, respectively, under the Amended and Restated Cooperation Agreement (collectively, the "2026 March Deferred Amounts").

The effectiveness of the 2026 March Deferral Agreement and the respective covenants, agreements and obligations of each party under the 2026 March Deferral Agreement are subject to the Company obtaining the requisite approval of the 2026 March Deferral Agreement from shareholders in accordance with the requirements of applicable Canadian securities laws and Rule 14.33 and Rule 14A.36 of the Listing Rules. The Company will be seeking approval of the 2026 March Deferral Agreement from disinterested shareholders at the Company's upcoming AGM of shareholders, which will be held at a future date to be set by the Board.

The principal terms of the 2026 March Deferral Agreement are as follows:

Payment of the 2026 March Deferred Amounts will be deferred until August 31, 2027 (the "2026 March Deferral Agreement Deferral Date").

As consideration for the deferral of the 2026 March Deferred Amounts which relate to the payment obligations arising from the Convertible Debenture, the Company agreed to pay JDZF a deferral fee equal to 6.4% per annum on the outstanding balance of such 2026 March Deferred Amounts, commencing on the date on which each such 2026 March Deferred Amounts would otherwise have been due and payable under the Convertible Debenture.

As consideration for the deferral of the 2026 March Deferred Amounts which relate to payment obligations arising from the Amended and Restated Cooperation Agreement, the Company agreed to pay JDZF a deferral fee equal to 1.5% per annum on the outstanding balance of such 2026 March Deferred Amounts commencing on the date on which each such 2026 March Deferred Amounts would otherwise have been due and payable under the Amended and Restated Cooperation Agreement.

The 2026 March Deferral Agreement does not contemplate a fixed repayment schedule for the 2026 March Deferred Amounts or related deferral fees. Instead, the 2026 March Deferral Agreement requires the Company to use its best efforts to pay the 2026 March Deferred Amounts and related deferral fees due and payable under the 2026 March Deferral Agreement to JDZF. During the period beginning as of the effective date of the 2026 March Deferral Agreement and ending as of the 2026 March Deferral Agreement Deferral Date, the Company will provide JDZF with monthly updates of its financial status and business operations, and the Company and JDZF will on a monthly basis discuss and assess in good faith the amount (if any) of the 2026 March Deferred Amounts and related deferral fees that the Company may be able to repay to JDZF, having regard to the working capital requirements of the Company's operations and business at such time and with the view of ensuring that the Company's operations and business would not be materially prejudiced as a result of any repayment.

If at any time before the 2026 March Deferred Amounts and related deferral fees are fully repaid, the Company proposes to appoint, replace or terminate one or more of its chief executive officer, its chief financial officer or any other senior executive(s) in charge of its principal business function or its principal subsidiary, the Company will first consult with, and obtain written consent (such consent shall not be unreasonably withheld) from JDZF prior to effecting such appointment, replacement or termination.

Going Concern - Several adverse conditions and material uncertainties relating to the Company cast significant doubt upon the going concern assumption which includes the deficiencies in assets and working capital.

See section "Liquidity and Capital Resources" of this press release for details.

OVERVIEW OF OPERATIONAL DATA AND FINANCIAL RESULTS

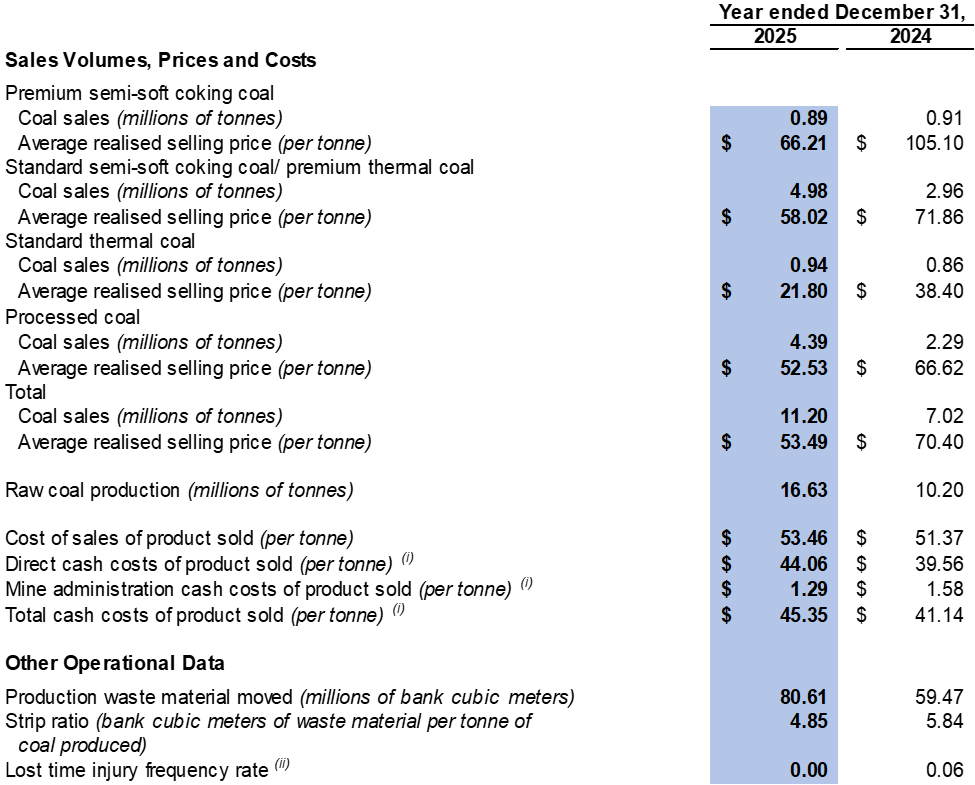

Summary of Annual Operational Data

A Non-International Financial Reporting Standards ("non-IFRS") financial measure. Refer to "Non-IFRS Financial Measures" section. Cash costs of product sold exclude idled mine asset cash costs.

Per 200,000 man hours and calculated based on a rolling 12 month average.

Overview of Annual Operational Data

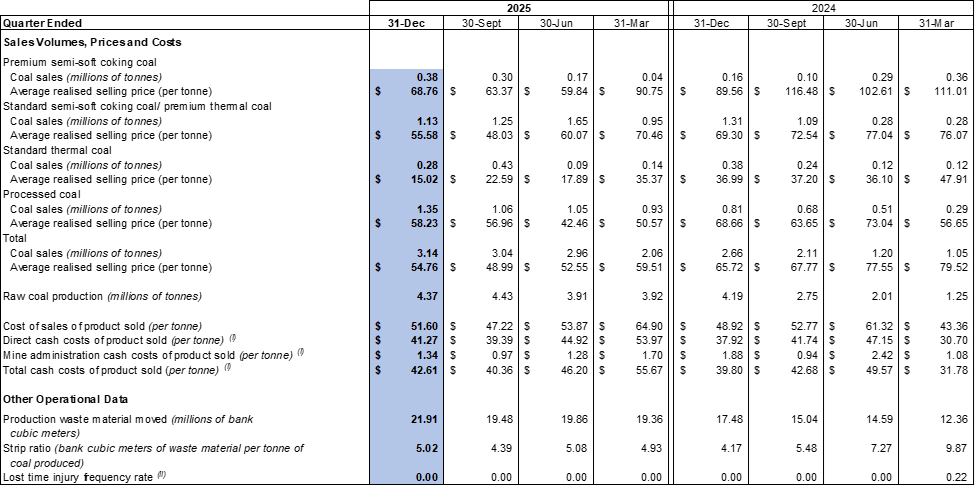

The Company recorded an average realised selling price of $53.5 per tonne in 2025 compared to $70.4 per tonne in 2024. The decrease was mainly due to the Company facing headwinds in the China coal market since 2024, leading to the Company changing its product mix to sell a greater percentage of lower-priced coal products. The product mix for 2025 consisted of approximately 8% of premium semi-soft coking coal, 45% of standard semi-soft coking coal/premium thermal coal, 8% of standard thermal coal and 39% of processed coal compared to approximately 13% of premium semi-soft coking coal, 42% of standard semi-soft coking coal/premium thermal coal, 12% of standard thermal coal and 33% of processed coal for 2024.

The Company's unit cost of sales of product sold was $53.5 per tonne in 2025 compared to $51.4 per tonne in 2024. The increase was due to the change in product mix year-over-year, as the Company sold more processed coal with higher production costs.

There was no lost time injury recorded in 2025, while there was a lost time injury frequency rate of 0.06 in 2024.

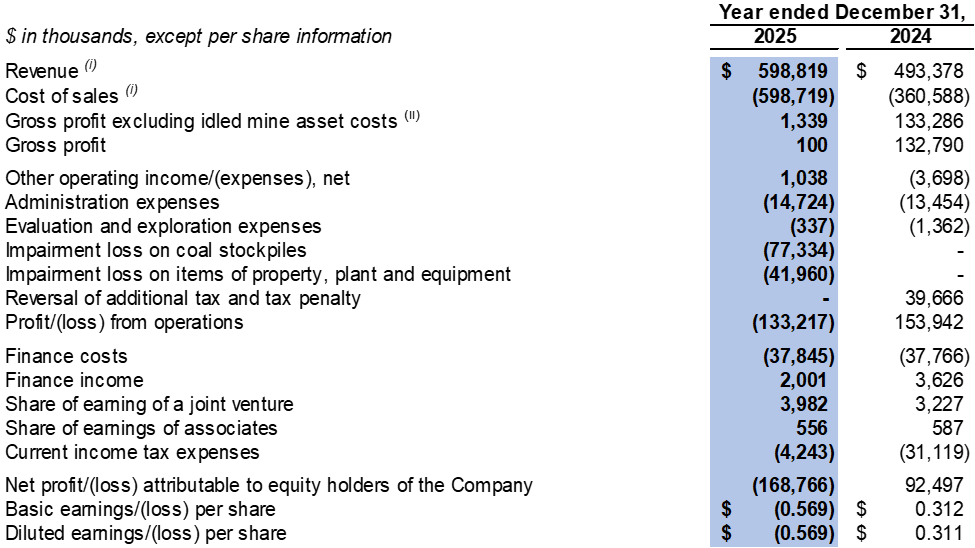

Summary of Annual Financial Results

Revenue and cost of sales related to the Company's Ovoot Tolgoi Mine within the Coal Division operating segment. Refer to note 2 of the selected information from the notes to the consolidated financial statements in this press release for further analysis regarding the Company's reportable operating segments.

A non-IFRS financial measure, idled mine asset costs represents the depreciation expense relates to the Company's idled plant and equipment.

Overview of Annual Financial Results

The Company recorded a $133.2 million loss from operations in 2025 compared to $153.9 million profit from operations in 2024. The decrease was mainly due to the decreased average realised selling price in 2025 as compared to 2024, the change in product mix year-over-year (as the Company sold more processed coal with higher production costs) and impairment losses on coal stockpile and items of property, plant and equipment of $77.3 million and $42.0 million were recorded respectively in 2025.

Revenue was $598.8 million in 2025 compared to $493.4 million in 2024. The financial results were impacted by increased sales volume year-over-year, as a result of an expansion of the Company's sales network, diversification of its customer baseand expansion of the categories of coal products in its portfolio.

Cost of sales was $598.7 million in 2025 compared to $360.6 million in 2024. The increase in cost of sales was mainly due to increased sales volume year-over-year, the Company expanding into certain categories of processed coal with higher production costs and more sales were made to a farther destination with higher transportation cost.

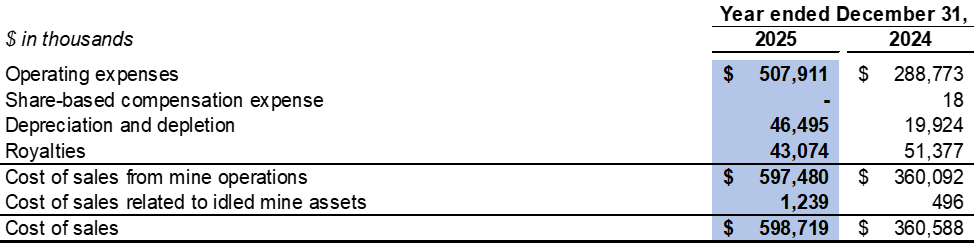

Cost of sales consists of operating expenses, share-based compensation expense, equipment depreciation, depletion of mineral properties, royalties and idled mine asset costs. Operating expenses in cost of sales reflect the total cash costs of product sold (a Non-IFRS financial measure, refer to "Non-IFRS Financial Measures" section of this press release for further analysis) during the year.

Operating expenses in cost of sales were $507.9 million in 2025 compared to $288.8 million in 2024. The overall increase in operating expenses was due to the Company expanding into certain categories of processed coal with higher production costs and more sales were made to a farther destination with higher transportation cost.

Cost of sales related to idled mine assets in 2025 included $1.2 million related to depreciation expenses for idled equipment (2024: $0.5 million).

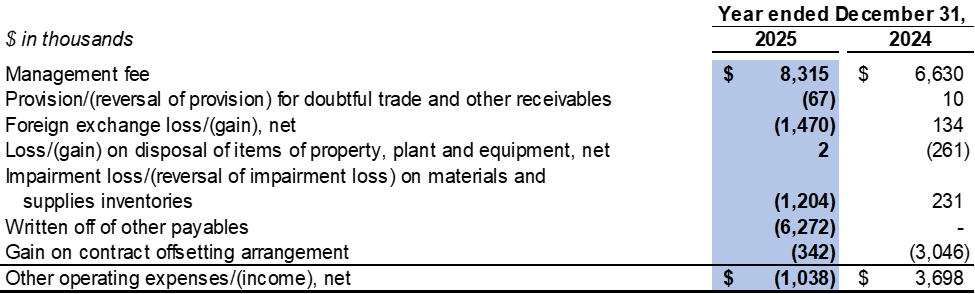

Other operating income was $1.0 million in 2025 as compared to other operating expenses of $3.7 million in 2024. The amount mainly consisted of foreign exchange gain of $1.5 million, reversal of impairment loss on materials and supplies inventories of $1.2 million and written off of other payables of $6.3 million, which was offset by management fee of $8.3 million.

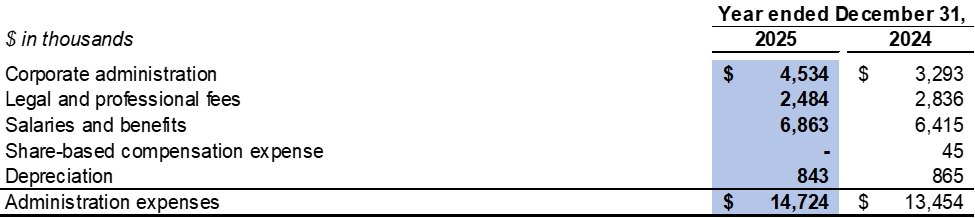

Administration expenses were $14.7 million in 2025 as compared to $13.5 million in 2024. The change was mainly due to higher daily administration fees and increased salaries and benefits as a result of an expansion of operations.

The Company continued to minimise evaluation and exploration expenditures in 2025 in order to preserve the Company's financial resources. Evaluation and exploration activities and expenditures in 2025 were limited to ensuring that the Company met the Mongolian Minerals Law requirements in respect of its mining licenses.

Finance costs were $37.8 million in both 2025 and 2024, which primarily consisted of interest expense on the $250.0 million Convertible Debenture.

Summary of Quarterly Operational Data

A non-IFRS financial measure. Refer to section "Non-IFRS Financial Measures". Cash costs of product sold exclude idled mine asset cash costs.

Per 200,000 man hours and calculated based on a rolling 12 month average.

Overview of Quarterly Operational Data

The Company experienced a decrease in the average selling price of coal from $65.7 per tonne in the fourth quarter of 2024 to $54.8 per tonne in the fourth quarter of 2025, as a result of the Company facing headwinds in the China coal market in 2025. This led the Company to change its product mix to sell a greater percentage of lower-priced coal products. The product mix for the fourth quarter of 2025 consisted of approximately 12% premium semi-soft coking coal, 36% standard semi-soft coking coal/premium thermal coal, 9% standard thermal coal and 43% of processed coal compared to approximately 6% premium semi-soft coking coal, 49% standard semi-soft coking coal/premium thermal coal, 14% standard thermal coal and 31% of processed coal in the fourth quarter of 2024.

The Company sold 3.1 million tonnes for the fourth quarter of 2025, compared to 2.7 million tonnes for the fourth quarter of 2024.

The Company's unit cost of sales of product sold increased from $48.9 per tonne in the fourth quarter of 2024 to $51.6 per tonne in the fourth quarter of 2025. The increase was mainly due to the Company expanding into certain categories of processed coal with higher production costs.

Summary of Quarterly Financial Results

The Company's annual financial statements are reported under the IFRS Accounting Standards. The following table provides highlights, extracted from the Company's annual and interim consolidated financial statements, of quarterly financial results for the past eight quarters.

Revenue and cost of sales relate to the Company's Ovoot Tolgoi Mine within the Coal Division operating segment. Refer to note 2 of the selected information from the notes to the consolidated financial statements in this press release for further analysis regarding the Company's reportable operating segments.

A non-IFRS financial measure, idled mine asset costs represents the depreciation expense relates to the Company's idled plant and equipment.

Overview of Quarterly Financial Results

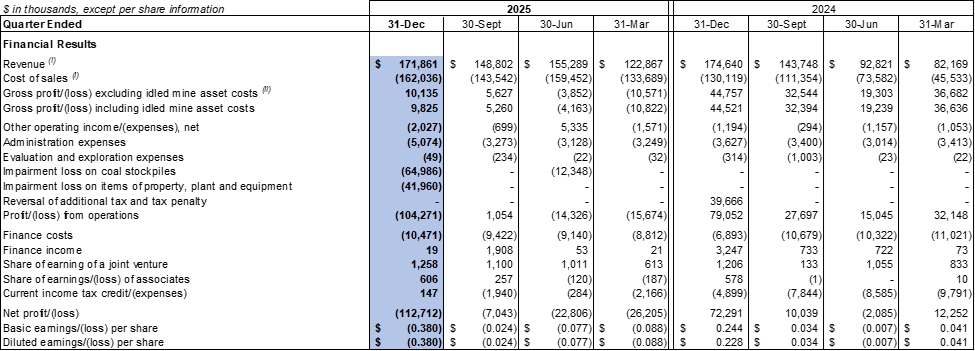

The Company recorded a $104.3 million loss from operations in the fourth quarter of 2025 compared to a $79.1 million profit from operations in the fourth quarter of 2024. The decrease was mainly due to the decreased average realised selling price realised in the fourth quarter of 2025 as compared to the same period in 2024, change in product mix, as the Company sold more processed coal with higher production costs and impairment losses on coal stockpile and items of property, plant and equipment of $65.0 million and $42.0 million were recorded respectively in the fourth quarter of 2025.

Revenue was $171.9 million in the fourth quarter of 2025 compared to $174.6 million in the fourth quarter of 2024. The Company was able to maintain its revenue amount as a result of an expansion of its sales network, diversification of its customer base and expansion of the categories of coal products in its portfolio.

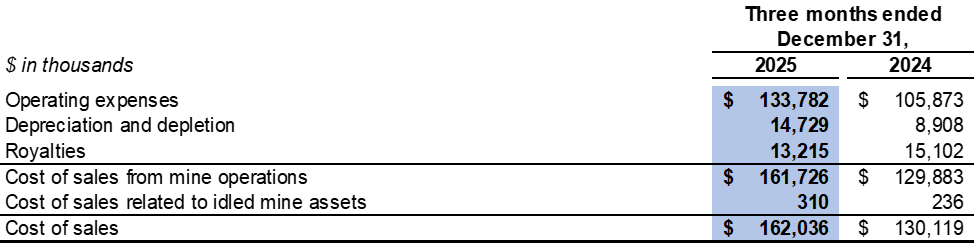

Cost of sales was $162.0 million in the fourth quarter of 2025 compared to $130.1 million in the fourth quarter of 2024. The increase in cost of sales was mainly due to increased sales volume, the Company expanding into certain categories of processed coal with higher production costs and the increase in sales made to further destinations with higher transportation cost.

Cost of sales consists of operating expenses, share-based compensation expense, equipment depreciation, depletion of mineral properties, royalties and idled mine asset costs. Operating expenses in cost of sales reflect the total cash costs of product sold (a Non-IFRS financial measure, refer to section "Non-IFRS Financial Measures" for further analysis) during the quarter.

Operating expenses in cost of sales were $133.8 million for the fourth quarter of 2025 compared to $105.9 million for the fourth quarter of 2024. The overall increase in operating expenses was due to the Company expanding into certain categories of processed coal with higher production costs and the increase in sales were made to further destinations with higher transportation cost.

Cost of sales related to idled mine assets in the fourth quarter of 2025 included $0.3 million related to depreciation expenses for idled equipment (fourth quarter of 2024: $0.2 million).

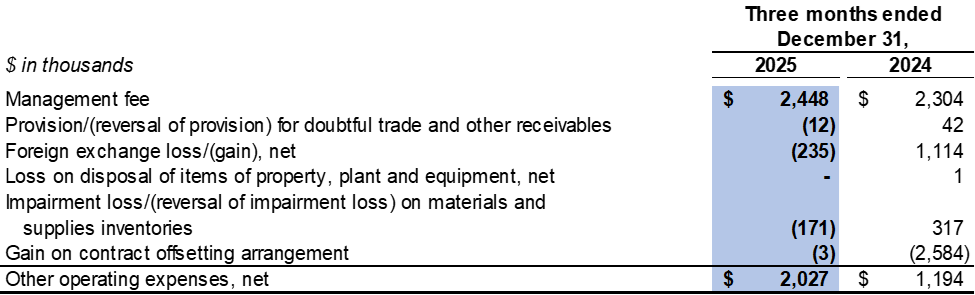

Other operating expenses were $2.0 million for the fourth quarter of 2025 compared to $1.2 million for the fourth quarter of 2024.

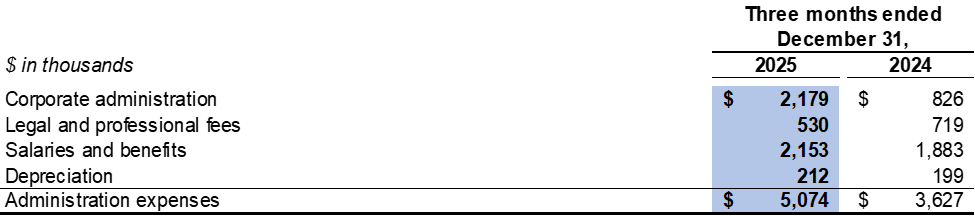

Administration expenses were $5.1 million in the fourth quarter of 2025 compared to $3.6 million in the fourth quarter of 2024. The change was mainly due to an increase in daily administration expenses and salaries and benefits as a result of an expansion of operations.

The Company continued to minimise evaluation and exploration expenditures in the fourth quarter of 2025 in order to preserve the Company's financial resources. Evaluation and exploration activities and expenditures in the fourth quarter of 2025 were limited to ensuring that the Company met the Mongolian Minerals Law requirements in respect of its mining licenses.

Finance costs were $10.5 million in the fourth quarter of 2025 compared to $6.9 million in the fourth quarter of 2024, which primarily consisted of interest expense on the $250.0 million Convertible Debenture.

LIQUIDITY AND CAPITAL RESOURCES

Liquidity and Capital Management

The Company has in place a planning, budgeting and forecasting process to help determine the funds required to support the Company's normal operations on an ongoing basis and the Company's expansionary plans.

Bank Loan

On October 7, 2025, SGS has entered into the 2025 Bank Loan for a principal amount of up to RMB235 million (equivalent to approximately $33.1 million) from the Bank with the key commercial terms as follows:

Maturity date set at 18 months from drawdown;

Interest rate of 10% per annum on the outstanding principal and interest is calculated on a 365-day year basis;

Loan repayments will consist of interest-only payments during the initial 12 months of the Term, followed by principal amortisation payments during months 13 to 18 of the Term;

Certain items of property, plant and equipment with carrying amount of $2.2 million, land-use rights and intangible assets were pledged as security for the 2025 Bank Loan; and

The Company intends to use the proceeds of the 2025 Bank Loan to support working capital, operating expenses, taxes and the settlement of accounts payable of SGS.

Additional tax and tax penalty imposed by the MTA

On July 18, 2023, SGS received the Notice issued by the MTA stating that the MTA had completed the Audit on the financial information of SGS for the tax assessment years between 2017 and 2020, including transfer pricing, royalty, air-pollution fee and unpaid tax payables. As a result of the Audit, the MTA notified SGS that it is imposing a tax penalty against SGS in the amount of approximately $75.0 million. The penalty mainly relates to the different view on the interpretation of tax law between the Company and the MTA. Under Mongolian law, the Company had a period of 30 days from the date of receipt of the Notice to file an appeal in relation to the Audit. Subsequently the Company engaged an independent tax consultant in Mongolia to provide tax advice and support to the Company and filed an appeal letter in relation to the Audit with the MTA in accordance with Mongolian laws on August 17, 2023.

On February 8, 2024, SGS received notice from the TDRC which stated that, after the TDRC's review, the TDRC issued a decision in relation to SGS' appeal of the Audit, and ordered that the audit assessments set forth in the Notice of July 18, 2023 be sent back to the MTA for review and re-assessment.

On February 22, 2024, SGS received another notice from the MTA stating that the MTA anticipated commencing the re-assessment process on or about March 7, 2024 and the duration of such process will be approximately 45 working days.

On May 15, 2024, SGS received the Revised Notice from the MTA regarding the Re-assessment Result. The re-assessed amount of the tax penalty is approximately $80.0 million. In accordance with applicable Mongolian laws, SGS is entitled to file an appeal to the TDRC regarding the Re-assessment Result within a 30-day period from the date of receiving the Revised Notice.

On June 12, 2024, following consultation with its independent tax consultant in Mongolia, SGS submitted an appeal letter to the TDRC regarding the Re-assessment Result, in accordance with applicable Mongolian laws.

On January 10, 2025, SGS received the Resolution from the TDRC in response to the appeal letter sent by SGS to the TDRC on June 12, 2024, relating to the Re-assessment Result. As set forth in the Resolution, the TDRC has determined to reduce the re-assessed amount of tax penalty against SGS from approximately $80.0 million to approximately $26.5 million. In accordance with applicable Mongolian laws, SGS is entitled to file an appeal to the Administrative Court of First Instance regarding the Revised Re-assessment Result within a 30-day period from the date of receiving the Resolution. After careful consideration and consultation with the Company's independent tax consultant in Mongolia, the Company has determined not to pursue a further appeal of the Revised Re-assessment Result with the Administrative Court of First Instance.

On March 19, 2025, SGS received correspondence from the Administrative Court of First Instance requesting supplemental information regarding a court proceeding initiated by the MTA Officials against the TDRC. Upon further enquiry, SGS obtained a copy of an order dated March 7, 2025 issued by the Administrative Court of First Instance regarding the Proposed Case.

On April 25, 2025, SGS obtained a copy of the Latest Court Order issued by the Administrative Court of First Instance refusing to accept the Proposed Case. According to the Latest Court Order, the Proposed Case was dismissed by the Administrative Court of First Instance. According to applicable Mongolian laws, the plaintiff is entitled to file an appeal to the appellate court, and the Company understood that the MTA Officials, as plaintiff in the Proposed Case, filed an appeal.

On June 9, 2025, SGS obtained the Appellate Court Judgement issued by the Appellate Court. As per the Appellate Court Judgement, the Appellate Court upheld the court order issued by the Judge of the Administrative Court of First Instance on April 15, 2025. As a result, the claim brought by the MTA Officials against the TDRC in an attempt to dispute or overturn the previous decision made by the TDRC regarding the Re-assessment Result has been dismissed and rejected. According to applicable Mongolian law, the Appellate Court Judgement shall be final and is not subject to further appeal.

In the prior year, the Company recorded an additional tax and tax penalty in the amount of $45.5 million, which consists of a tax penalty payable of $26.5 million and a provision for additional late tax penalty of $19.0 million. As a result of the Revised Re-assessment Result, the Company recorded a reversal of additional tax and tax penalty of $48.5 million in 2024. To date, the Company has paid the MTA an aggregate of $22.2 million in relation to the aforementioned tax penalty. The Company anticipates paying down the outstanding amount of the tax and tax penalty from cash generated from operations in the normal course. According to Mongolian tax law, the MTA has a legal authority to demand payment of the outstanding amount of the Revised Re-assessment Result from the Company at its discretion.

Going concern considerations

The Company's consolidated financial statements have been prepared on a going concern basis which assumes that the Company will continue to operate until at least December 31, 2026 and will be able to realise its assets and discharge its liabilities in the normal course of operations as they come due. However, in order to continue as a going concern, the Company must generate sufficient operating cash flows, secure additional capital or otherwise pursue a strategic restructuring, refinancing or other transactions to provide it with sufficient liquidity.

Several adverse conditions and material uncertainties cast significant doubt upon the Company's ability to continue as a going concern and the going concern assumption used in the preparation of the Company's consolidated financial statements. The Company had a deficiency in assets of $227.2 million as at December 31, 2025 as compared to a deficiency in assets of $49.8 million as at December 31, 2024 while the working capital deficiency (excess current liabilities over current assets) reached $337.0 million as at December 31, 2025 as compared to a working capital deficiency of $228.1 million as at December 31, 2024.

Included in the working capital deficiency as at December 31, 2025 are significant obligations, represented by trade and other payables of $218.2 million, additional tax and tax penalty of $23.3 million and interest-bearing borrowing of $11.1 million.

The Company may not be able to settle all trade and other payables on a timely basis, and as a result any continuing postponement in settling of certain trade and other payables owed to suppliers and creditors may result in potential lawsuits and/or bankruptcy proceedings being filed against the Company. Except as disclosed elsewhere in this press release, no such lawsuits or proceedings were pending as at March 27, 2026. However, there can be no assurance that no such lawsuits or proceedings will be filed by the Company's creditors in the future and the Company's suppliers and contractors will continue to supply and provide services to the Company uninterrupted.

In addition, the recent global geopolitical events, particularly the escalation of tensions involving Iran and the US, have significantly pushed up international coal prices in the short term due to increasing energy prices and demand for coal as a substitute for natural gas. However, management notes that coal price trends remain subject to uncertainties related to the duration of such conflicts and broader geopolitical developments. Should the conflict ease or cease, the price momentum driven by supply risk premiums and energy substitution may weaken or even reverse, thereby exposing coal prices to considerable downside uncertainty. Such volatility may affect the Company's operations, including the selling price of its coal product and its production costs.

There are significant uncertainties as to the outcomes of the above events or conditions that may cast significant doubt on the Company's ability to continue as a going concern and, therefore, the Company may be unable to realise its assets and discharge its liabilities in the normal course of business. Should the use of the going concern basis in preparation of the consolidated financial statements be determined to be not appropriate, adjustments would have to be made to write down the carrying amounts of the Company's assets to their realisable values, to provide for any further liabilities which might arise and to reclassify non-current assets and non-current liabilities as current assets and current liabilities, respectively. The effects of these adjustments have not been reflected in the consolidated financial statements. If the Company is unable to continue as a going concern, it may be forced to seek relief under applicable bankruptcy and insolvency legislation.

For the purpose of assessing the appropriateness of the use of the going concern basis to prepare the consolidated financial statements, management of the Company has prepared a cash flow projection covering a period of 12 months from December 31, 2025. The cash flow projection has considered the anticipated cash flows to be generated from the Company's business during the period under projection including cost saving measures. In particular, the Company has taken into account the following measures for improvement of the Company's liquidity and financial position, which include: (a) entering into the 2026 March Deferral Agreement on March 23, 2026 for a deferral of the 2026 March Deferred Amounts; (b) communicating with vendors in agreeing repayment plans of the outstanding payable; and (c) considering geopolitical tensions, specifically the Iran-US conflict, which is expected to create a favourable pricing environment during forecast period. Regarding these plans and measures, there is no guarantee that the suppliers would agree the settlement plan as communicated by the Company. Nevertheless, after considering the above, the directors of the Company believe that there will be sufficient financial resources to continue its operations and to meet its financial obligations as and when they fall due in the next 12 months from December 31, 2025 and therefore are satisfied that it is appropriate to prepare the consolidated financial statements on a going concern basis.

Significant uncertainties exist regarding the Company's management's ability to achieve its plans as described above. The continued operation of the Company as a going concern depends on the following key factors: the utilisation of financial support from an affiliate of the Company's major shareholder to settle payables, including the additional tax and tax penalty, in a timely manner, and the fluctuations in international coal prices, which are subject to the developments in geopolitical tensions.

The outcome of this factor will have a significant impact on the Company's ability to continue operating as a going concern. It is crucial to closely monitor and address these uncertainties to ensure the Company's stability and long-term viability.

Factors that impact the Company's liquidity are being closely monitored and include, but are not limited to, restrictions on the Company's ability to import its coal products for sale in China, Chinese economic growth, market prices of coal, production levels, operating cash costs, capital costs, exchange rates of currencies of countries where the Company operates and exploration and discretionary expenditures.

As at December 31, 2025, the Company was not subject to any externally imposed capital requirements.

Convertible Debenture

In November 2009, the Company entered into a financing agreement with China Investment Corporation (together with its wholly-owned subsidiaries and affiliates, "CIC") for $500 million in the form of a secured, convertible debenture bearing interest at 8.0% (6.4% payable semi-annually in cash and 1.6% payable annually in the Company's Common Shares) with a maximum term of 30 years. The Convertible Debenture is secured by a first ranking charge over the Company's assets, including shares of its material subsidiaries. The financing was used primarily to support the accelerated investment program in Mongolia and for working capital, repayment of debts, general and administrative expenses and other general corporate purposes.

On March 29, 2010, the Company exercised its right to call for the conversion of up to $250.0 million of the Convertible Debenture into approximately 21.5 million shares at a conversion price of $11.64 (CA$11.88).

Deferral Agreements

2024 March Deferral Agreement

On March 19, 2024, the Company and JDZF entered into an agreement (the "2024 March Deferral Agreement") pursuant to which JDZF agreed to grant the Company a deferral of (i) the cash and PIK Interest, management fees, and related deferral fees in the aggregate amount of approximately $96.5 million due and payable to JDZF on or before August 31, 2024 pursuant to certain prior deferral agreements dated March 24, 2023 and October 13, 2023; (ii) semi-annual cash interest payment of approximately $7.9 million payable to JDZF on May 19, 2024 under the Convertible Debenture; (iii) semi-annual cash interest payments of approximately $8.1 million payable to JDZF on November 19, 2024 and the $4.0 million in PIK Interest payable to JDZF on November 19, 2024 under the Convertible Debenture; and (iv) management fees in the aggregate amount of $2.2 million payable to JDZF on November 15, 2024 and February 15, 2025, respectively, under the Amended and Restated Cooperation Agreement (collectively, the "2024 March Deferred Amounts").

The effectiveness of the 2024 March Deferral Agreement and the respective covenants, agreements and obligations of each party under the 2024 March Deferral Agreement are subject to the Company obtaining the requisite approval of the 2024 March Deferral Agreement from shareholders in accordance with the requirements of applicable Canadian securities laws and Rule 14.33 and Rule 14A.36 of the Listing Rules. The 2024 March Deferral Agreement was approved by the Company's disinterested shareholders through a special meeting of shareholders convened on August 28, 2024.

The principal terms of the 2024 March Deferral Agreement are as follows:

Payment of the 2024 March Deferred Amounts are deferred until August 31, 2025 (the" 2024 March Deferral Agreement Deferral Date").

As consideration for the deferral of the 2024 March Deferred Amounts which relate to the payment obligations arising from the Convertible Debenture, the Company agreed to pay JDZF a deferral fee equal to 6.4% per annum on the outstanding balance of such 2024 March Deferred Amounts, commencing on the date on which each such 2024 March Deferred Amounts would otherwise have been due and payable under the Convertible Debenture.

As consideration for the deferral of the 2024 March Deferred Amounts which relate to payment obligations arising from the Amended and Restated Cooperation Agreement, the Company agreed to pay JDZF a deferral fee equal to 1.5% per annum on the outstanding balance of such 2024 March Deferred Amounts commencing on the date on which each such 2024 March Deferred Amounts would otherwise have been due and payable under the Amended and Restated Cooperation Agreement.

The 2024 March Deferral Agreement does not contemplate a fixed repayment schedule for the 2024 March Deferred Amounts or related deferral fees. Instead, the 2024 March Deferral Agreement requires the Company to use its best efforts to pay the 2024 March Deferred Amounts and related deferral fees due and payable under the 2024 March Deferral Agreement to JDZF. During the period beginning as of the effective date of the 2024 March Deferral Agreement and ending as of the 2024 March Deferral Agreement Deferral Date, the Company will provide JDZF with monthly updates of its financial status and business operations, and the Company and JDZF will on a monthly basis discuss and assess in good faith the amount (if any) of the 2024 March Deferred Amounts and related deferral fees that the Company may be able to repay to JDZF, having regard to the working capital requirements of the Company's operations and business at such time and with the view of ensuring that the Company's operations and business would not be materially prejudiced as a result of any repayment.

If at any time before the 2024 March Deferred Amounts and related deferral fees are fully repaid, the Company proposes to appoint, replace or terminate one or more of its chief executive officer, its chief financial officer or any other senior executive(s) in charge of its principal business function or its principal subsidiary, the Company will first consult with, and obtain written consent (such consent shall not be unreasonably withheld) from JDZF prior to effecting such appointment, replacement or termination.

2024 April Deferral Agreement

On April 30, 2024, the Company and JDZF entered into an agreement (the "2024 April Deferral Agreement") pursuant to which JDZF agreed to grant the Company a deferral of the remaining $1.1 million of PIK interest which was payable on November 19, 2022 under the Convertible Debenture, the payment of which was deferred pursuant to a certain prior deferral agreement dated November 11, 2022 (the "November 2022 Deferral Agreement") until November 19, 2023, as well as related deferral fees under the November 2022 Deferral Agreement (collectively, the "2024 April Deferred Amounts").

The effectiveness of the 2024 April Deferral Agreement and the respective covenants, agreements and obligations of each party under the 2024 April Deferral Agreement are subject to the Company obtaining the requisite approval of the 2024 April Deferral Agreement from shareholders in accordance with the requirements of applicable Canadian securities laws and Rule 14.33 and Rule 14A.36 of the Listing Rules. The 2024 April Deferral Agreement was approved by the Company's disinterested shareholders through a special meeting of shareholders convened on August 28, 2024.

The principal terms of the 2024 April Deferral Agreement are as follows:

Payment of the 2024 April Deferred Amounts are deferred until August 31, 2025 (the" 2024 April Deferral Agreement Deferral Date").

As consideration for the deferral of the 2024 April Deferred Amounts, the Company agreed to pay JDZF a deferral fee equal to 6.4% per annum on the outstanding balance of such 2024 April Deferred Amounts, commencing on the date on which each such 2024 April Deferred Amounts would otherwise have been due and payable under the Convertible Debenture.

The 2024 April Deferral Agreement does not contemplate a fixed repayment schedule for the 2024 April Deferred Amounts or related deferral fees. Instead, the 2024 April Deferral Agreement requires the Company to use its best efforts to pay the 2024 April Deferred Amounts and related deferral fees due and payable under the 2024 April Deferral Agreement to JDZF. During the period beginning as of the effective date of the 2024 April Deferral Agreement and ending as of the 2024 April Deferral Agreement Deferral Date, the Company will provide JDZF with monthly updates of its financial status and business operations, and the Company and JDZF will on a monthly basis discuss and assess in good faith the amount (if any) of the 2024 April Deferred Amounts and related deferral fees that the Company may be able to repay to JDZF, having regard to the working capital requirements of the Company's operations and business at such time and with the view of ensuring that the Company's operations and business would not be materially prejudiced as a result of any repayment.

If at any time before the 2024 April Deferred Amounts and related deferral fees are fully repaid, the Company proposes to appoint, replace or terminate one or more of its chief executive officer, its chief financial officer or any other senior executive(s) in charge of its principal business function or its principal subsidiary, the Company will first consult with, and obtain written consent (such consent shall not be unreasonably withheld) from JDZF prior to effecting such appointment, replacement or termination.

2025 March Deferral Agreement

On March 20, 2025, the Company and JDZF entered into the 2025 March Deferral Agreement pursuant to which JDZF agreed to grant the Company a deferral of the 2025 March D